Current situation 1: High growth in installed capacity

China is a rising star in the global new energy storage market. On January 25, 2024, the National Energy Administration held a press conference. According to data, as of the end of 2023, the cumulative installed capacity of new energy storage projects that have been completed and put into operation nationwide has reached 31.39 million kilowatts/66.87 million kilowatt hours, with an average energy storage time of 2.1 hours. The newly added installed capacity in 2023 is about 22.6 million kilowatts/48.7 million kilowatt hours, an increase of over 260% compared to the end of 2022, and nearly 10 times the installed capacity at the end of the 13th Five Year Plan period.

According to the Guiding Opinions on Accelerating the Development of New Energy Storage issued by the National Development and Reform Commission and the National Energy Administration, by 2025, the installed capacity of new energy storage will reach over 30 million kilowatts. It can be seen that by the end of 2023, China's new energy storage has achieved its 2025 installation target ahead of schedule.

This is mainly due to the intensive introduction of favorable national policies, the increasing maturity of new energy storage business models, and the continuous reduction of initial investment costs in the system.

Current situation 2: Low price internal competition, with a decline close to halving

On one hand, there is a rapidly expanding production capacity, and on the other hand, there is a market that is slowly stalling. It is not difficult to find that the price war in the energy storage field began with the structurally surplus battery cell field, and then triggered a continuous decline in the price of DC side systems, followed by a continuous downward trend in the price war of AC side systems.

The average price of energy storage batteries has dropped from 0.9 yuan to 1.0 yuan/Wh at the beginning of 2023 to 0.4 yuan to 0.5 yuan/Wh at the end of the year, with prices directly halved. At the same time, compared to the beginning of the year, the average price of energy storage systems has dropped to about 0.8 yuan/Wh, a decrease of 40%, and is also close to halving.

Current situation 3: The path of energy storage IPO is experiencing a wave of withdrawal

In August 2023, the China Securities Regulatory Commission announced a phased tightening of the pace of IPOs (initial public offerings) to promote dynamic balance between investment and financing. Many energy storage companies are slowing down their IPO pace.

According to incomplete statistics, there will be nearly 400 investment and financing events related to energy storage in 2023, with a financing scale of over 100 billion yuan. There are over a hundred energy storage companies lining up for IPOs, and more than 20 companies have completed IPOs, but there are also over 20 energy storage related companies that have terminated their listings. The reason for online rumors is that the China Securities Regulatory Commission believes that some energy storage companies lack core competitiveness.

Current situation 4: Accelerated development of industrial and commercial energy storage

As the price difference between peak and valley in various regions of China continues to widen, coupled with the decrease in lithium battery costs, the IRR (internal rate of return) of industrial and commercial energy storage is steadily increasing, and its economic viability is becoming increasingly evident. Industrial and commercial energy storage has become the fastest-growing branch in the energy storage track. The installed capacity of commercial and industrial energy storage systems on the user side (lithium battery energy storage systems) is expected to approach 2GWh in 2023, and will continue to maintain a high growth rate from 2024 to 2025. It should be noted that the total size of this market in 2022 is only a few hundred MWh.

Industrial and commercial energy storage has attracted intensive capital inflows due to its explosive growth in the past two years. According to relevant data, since 2023, there have been over 50000 newly registered energy storage enterprises in China, with an average of over 150 new enterprises entering the energy storage field every day. In terms of installed capacity, from January to June 2023 alone, China's newly added industrial and commercial energy storage installed capacity reached 2826.7 kilowatt hours, a year-on-year increase of 1231%. The growth rate of industry scale/market demand cannot keep up with the growth rate of enterprise quantity/industry capacity.

2023 is widely recognized as the first year of industrial and commercial energy storage in the industry. Due to its wide range of application scenarios and the release of favorable policies such as peak and valley electricity prices and spot electricity prices, the industrial and commercial energy storage industry has seen a phenomenon of "rushing forward". However, influenced by time of use electricity pricing policies, subsidy policies, and industrial development foundations in different regions, the differences in the industrial and commercial energy storage market will continue to widen. In the short term, provinces and regions such as Jiangsu, Zhejiang, and Guangdong will occupy the vast majority of market demand, and some enterprises will take the lead in forming brand awareness and channel influence in regional markets.

Taking Zhejiang as an example, the Zhejiang Provincial Energy Bureau recently issued the "Guidelines for User Side Electrochemical Energy Storage Technology in Zhejiang Province", which is the first user side energy storage technology guideline in China. This is a signal, a regulation of market order, and a constraint on frequent chaos such as low price competition and construction without investment.

The current 5: The household savings market is rapidly declining

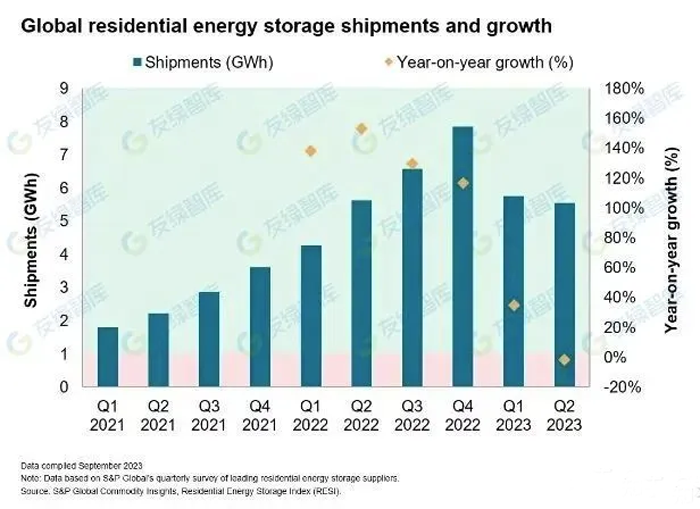

Since 2023, the accelerated cooling of the household storage market has become a recognized fact in the industry, which can be described as a "double-edged sword" compared to the prosperity of 2022. According to data from S&P Global, global shipments of household energy storage systems decreased year-on-year for the first time in the second quarter of 2023, marking the first recorded decline of 2% year-on-year.

The H1 shipment volume of household energy storage in 2023 is about 6GWh, with a significant downward adjustment in the annual forecast. Based on this, the first priority for household storage enterprises is to clear inventory. According to relevant statistics, the market size of household energy storage in Europe for the whole year of 2023 will reach 9.57GWh, and inventory digestion in the second half of the year will reach about 4.47GWh. It is expected that the clearance of household energy storage inventory will continue until the end of 2023 and the beginning of 2024.

Current situation 6: Energy storage cells iterate from 280Ah to 300+Ah

With the increasingly booming energy storage market, energy storage battery products are developing towards large capacity. By 2023, 280Ah square batteries will rapidly penetrate the market with their large capacity, high safety, high energy density, and mature mass production processes. Starting from 2023, in order to adapt to the trend of larger scale and capacity in the future energy storage market, the energy storage market will mainly focus on competing in 300Ah+large capacity batteries. By the end of 2023, nearly 30 domestic battery manufacturers including CATL, EVE Energy, Honeycomb Energy, Ruipu Lanjun, Nandu Power, Penghui Energy, Haichen Energy Storage, and Ganfeng Lithium have successively launched battery cell products with a capacity of over 300Ah.

The intensive launch of 300Ah+energy storage batteries reflects the positive growth and technological iteration of the energy storage market. Furthermore, in order to lay out future markets, some battery companies have already launched technological reserves such as 500Ah+, 600Ah+, 1000Ah+, and blade batteries.

Current situation 7: Competition for 20 foot 5MWh liquid cooled energy storage system

Along with the increase in battery capacity, the era of 5MWh+energy storage systems has also arrived. In 2023, at least 20 energy storage companies will successively release 20 foot 5MWh energy storage systems based on 314Ah/320Ah large battery cells.

The scale of energy storage units has increased, the number of parallel battery clusters has increased, and issues such as battery heat dissipation and balance have become prominent. The requirements for safety and temperature control technology are also higher, and liquid cooling solutions are replacing air cooling as the mainstream cooling technology for energy storage systems. In 2023, there is no doubt about the dispute between air cooling and liquid cooling, and liquid cooling has become a hot topic for major manufacturers to launch liquid cooling products. According to GGII's forecast, the market share of liquid cooling solutions will exceed 50% by 2025.

Current situation 8: Energy storage going global, brewing new changes in the global track

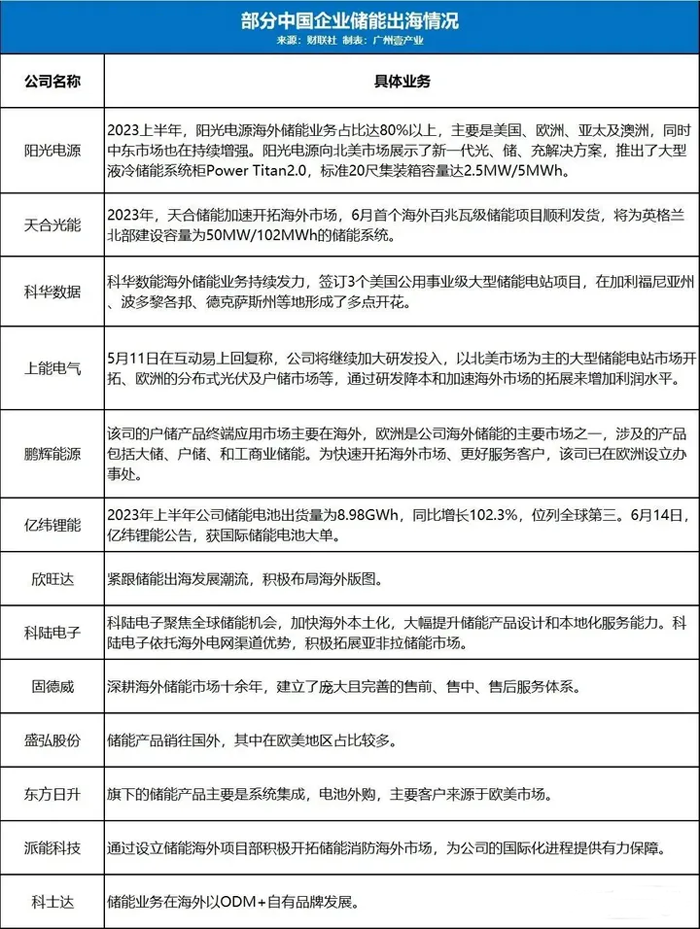

Going abroad has become the keyword for energy storage. From a global market perspective, China, the United States, and Europe are currently the top three energy storage markets in the world. According to the European Energy Storage Association, around 200GW of energy storage will need to be deployed by 2030, which means an additional 14GW will be added annually; By 2050, 600GW of energy storage needs to be deployed, which means an additional 20GW will be added annually after 2030. In terms of overseas markets, analysts say that the European and American markets have become an important business layout direction for China's top energy storage industry chain enterprises due to their high degree of electricity marketization and good profitability. The listed companies that have established energy storage related businesses overseas are mainly Sunac Power, Trina Solar, Kehua Data, Shangneng Electric, Penghui Energy, EVE Energy, Xinwangda, Kelu Electronics, Gudewei, Shenghong Shares, Dongfang Risheng, Paineng Technology, Keshida, etc.

Current situation 9: Grid based energy storage system enters the public eye for the first time

From 'following the grid' to 'building the grid', in 2023, grid based energy storage will initially enter the public eye. This requires the addition of new control strategies to the energy storage system on the new energy side, enabling it to have the frequency regulation and voltage control capabilities of synchronous generators or similar synchronous generators, forming a grid type energy storage system. The reason is that the proportion of new energy generation is rapidly increasing, and the power system is gradually showing the characteristics of "double high" (high proportion of renewable energy and high proportion of power electronic equipment). The production structure, operating mechanism, and functional form of the power system are undergoing profound changes, and problems such as low inertia, low damping, and weak voltage support are becoming prominent. The safe and stable operation of the power system is facing severe challenges.

Current situation 10: Commercialization of flow batteries accelerates

Flow batteries have inherent safety characteristics and have advantages in the field of energy storage with high safety requirements. Although flow batteries are in the early stages of commercialization, as the trend of long-term energy storage gradually becomes clear, the popularity of flow batteries only increases without decreasing. According to incomplete statistics, China's production capacity plan for flow batteries in 2023 has exceeded 90 GWh, with an investment amount of over 41.7 billion yuan and nearly 40 signed/under construction/put into operation projects. The development of flow batteries has significantly accelerated, and by 2025, the domestic shipment of flow batteries will exceed 10 GWh (calculated based on 4 hours, including exports), with a compound annual growth rate of over 90%.

Now, standing at the starting point of 2024, can we "clear the clouds and see the moonlight"? Based on the price war background, there will be four key points for energy storage development in 2024:

① Battery companies move from "rolled" battery cells to "rolled" systems

With battery companies joining the energy storage system integration track, industry competition has become increasingly fierce. Currently, many battery factories including CATL, BYD, EVE Energy Storage, Ruipu Lanjun, Haichen Energy Storage, and Honeycomb Energy are gradually entering the integration business. Battery cell manufacturers are developing new energy storage system products one after another. In addition to DC side products, many companies are also developing new AC side system products, with application scenarios covering power supply side, industrial and commercial side, user side, etc., directly participating in the competition in the energy storage field. If battery cell manufacturers transform into full system players, they may compete with existing customers and engage in comprehensive games across all aspects.

② Instead of internal competition, it's better to go out to sea

From the perspective of market share, the high demand in overseas markets has also led to more and more energy storage companies choosing to go abroad to seek a way out. In addition to the traditional mainstream energy storage markets in Europe, America, Australia and Japan, Southeast Asia, Africa and countries along the the Belt and Road have also become important target markets.

③ The energy storage industry is shifting from price driven to value driven, and there is a growing call for it to thrive

Behind the internal competition, the energy storage industry is accelerating towards value driven development, and the market is not seeking low prices, but true cost reduction capabilities. For example, in the industrial and commercial sector, the backend capabilities of energy storage enterprises are rapidly emerging, utilizing advanced technologies such as AI and big data analysis to enhance the profits of homeowners.

④ Exploring new incremental energy storage markets is underway

The first and foremost issue is that, in addition to the current energy storage fields such as new energy distribution and storage on the domestic power generation side and traditional user side, the application scenarios of industrial and commercial energy storage are constantly being explored. Again, continuously explore the scope of product usage and break through the upper limit of lithium battery application.